Created on 2026-05-11 23:34

Published on 2026-05-12 11:15

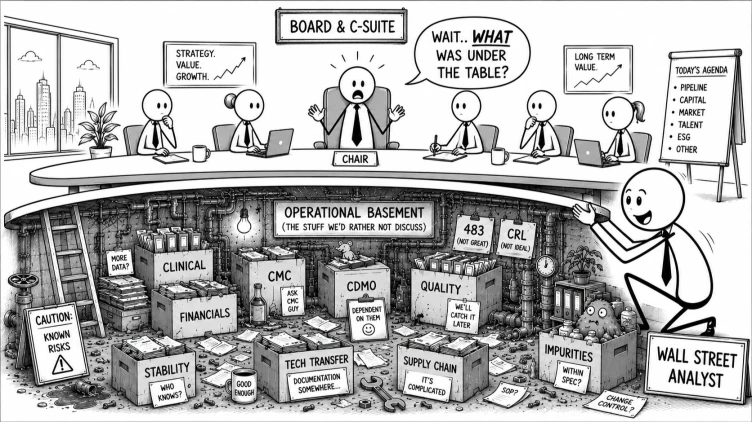

Wall Street has started reading CMCQ. CMC and Quality, in industry shorthand. The FDA’s Complete Response Letter archive has been public for ten months. This week, Jefferies and Mizuho both published quantitative reads of it. More than 50% of recent CRLs cite manufacturing. 41% cite product quality, including impurities and failed stability. 27% percent cite insufficient clinical data. The clinical bucket is the smaller bucket. The framework we publish on Thursday 14th is the operating model your board needs to govern against that pattern.

Is your board ready?

Jefferies’ Andrew Tsai concluded that sponsors are “seemingly more prepared when it comes to the clinical data package side of things vs CMC/manufacturing.” Mizuho framed it the same way. The Novo Nordisk Indiana facility that tripped Regeneron’s Eylea also tripped Scholar Rock’s apitegromab (kudos to their team for getting that resubmitted and the BLA accepted in record time). One CDMO site. Two sponsors. Two rejections. The board governance above each did not surface the underlying risk in advance. On Thursday at six in the morning Eastern, we publish the operating model that closes the gap between where CMCQ risk lives and where the board sees it. Free. With an offer to help you close the gap when you are ready.

The Jefferies analysis quantifies what CMC and Quality operators have been saying inside their companies for years. The dominant approval-blocking risk is now operational. The clinical bucket, while real, is smaller. Sponsors are demonstrably less prepared on CMCQ than on clinical. That asymmetry is now in research notes, which means the next earnings call, the next analyst day, and the next diligence meeting will surface CMCQ questions your board has to be ready to support the answers to.

The Novo Indiana case is the most legible illustration. Regeneron’s high-dose Eylea was rejected in October 2025 because of manufacturing violations at a Novo Nordisk facility. The FDA found atypical extrinsic particles in the plant, is this the agency’s language for pests and cat hair? The same facility, two months earlier, tripped Scholar Rock’s apitegromab. One CDMO. Two rejections. The risk lived in the manufacturing function was surfaced in the audit findings but the journey in between was not visible to the directors who should have been pricing the exposure.

If we're honest, would your board have asked, in 2024, whether your CMC strategy concentrated single-site risk on a CDMO whose 2025 inspection was already trending toward a Form 483? By observation, most boards do not have the language to ask that question but the framework that Phase 3 Search will publish on Thursday is built to give it to them.

The CRL data has been observable for a year. CMC operators have been talking about it. So has this audience. Over the last twelve months, the Phase 3 Search content engine has generated more than 600,000 impressions, reached more than 226,000 unique members, and produced 4,851 engagements across the portfolio. The April 21 runway piece on how boards evaluate their CTO is now the highest-impressions piece of the year at 45,174 impressions and 432 engagements. The case for treating CMCQ as a board-level governance category has been settled in this audience.

What is different this week is that the sell side has started pricing the pattern.

When Wall Street prices a risk category, the trickle-down is predictable. Within one to two quarters, strategic acquirers fold the same risk into term sheets, CVR structures, and milestone frameworks, because their diligence teams already do this work internally and now have research-note cover to act on it. Within two to four quarters, venture and crossover investors follow, because if Strategics are repricing acquisitions on CMCQ readiness, the earlier check has to underwrite that exit pricing or lose the multiple. And once VCs are asking portfolio companies to demonstrate readiness, boards are the ones who have to make sure the answer is yes.

The board chair who waits for the VC partner to ask about CMCQ preparedness has already missed the window. The board chair who reads Jefferies this week and acts on it is the one whose company exits at the multiple Wall Street will eventually demand.

At seven in the morning Eastern, we publish the CTO Mandate Framework. This is a combination of 1000s of observations from 13 years of executive search work, combined with the learnings of 17 Startup to Fortune 100 CTOs from some of our leading companies, between them they have launched upwards of 120 commercial products, and all of that wisdom is distilled into the operating model your board needs to govern CMC and Quality the way it already governs clinical, commercial, and financial risk.

It includes five lenses for evaluating technical leadership. A calibration tool that surfaces where board directors disagree about CMCQ emphasis and hard gates that should apply before the board commits to major capital events.

The CRL data is no longer information only the operators see. It is now in research notes.

If you sit on a biopharma board and you have ever felt that the CMCQ slide passed too quickly, this framework is for you.

If you are a crossover investor who has been writing CVRs to absorb operational risk you could not diligence, the framework is for you.

If you are a CMC or technical operations leader who has watched the boardroom questions stay shallow because no one knew which questions to ask, the framework is for you.

On Thursday it will be 8 years to the day that I started Phase 3 Search to honor a lost sibling and to materially change how medicine reaches patients.

It is that reason that the most important document I've ever produced will be free.

So, let's go do some good with it.

Every engagement begins with a diagnostic — a structured read on the role and the company you are actually inheriting.

Start a diagnostic