Created on 2026-04-25 00:26

Published on 2026-04-28 11:30

Pull up your board composition. Count the directors with clinical development experience. Count the ones with financial or capital markets backgrounds. Now count the ones who have personally managed a commercial manufacturing operation, built a quality system from the ground up, or sat across from an FDA investigator during a pre-approval inspection.

If the answer to that last question is zero, you are not unusual. You are the norm.

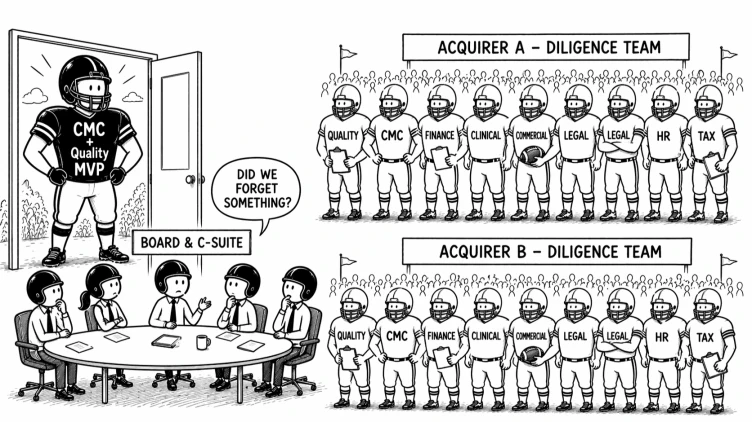

Now picture the diligence team your acquirer will send. They will staff it with CMC directors, quality VPs, regulatory operations leads -- people whose entire job is to find the manufacturing and quality gaps your board never asked about. They will arrive with more CMC expertise in a single conference room than your board has had in its entire history. And every gap they find becomes a purchase price adjustment, a contingent value right, or a deal term you didn't want to give.

That isn't bad luck. It's an information asymmetry your board composition created.

Biopharma boards are built around two competencies. The clinical lens evaluates pipeline risk -- trial design, regulatory strategy, probability of technical success. The financial lens evaluates capital risk -- burn rate, runway, dilution, exit timing. Both essential. Neither sufficient.

The third lens -- CMC and quality -- is the one most boards don't have. Not because they chose to leave it out, but because the default model of board construction doesn't include it. Meanwhile, 85% of small biopharma companies outsource API manufacturing and 77% outsource finished dose. The manufacturing and quality decisions that most affect valuation are increasingly made outside the company, in relationships no one on most boards has the experience to evaluate.

Inside operating companies, the market is already correcting for this. The emergence of the Chief Technical and Quality Officer -- the CTOQ -- reflects a growing recognition that manufacturing and quality are not separate functions that happen to coexist. They are two expressions of the same strategic discipline: ensuring that what the science creates can be made reliably, at scale, under regulatory scrutiny.

The traditional model separated these functions. The CTO owned process development and manufacturing. The VP or SVP of Quality owned compliance, deviations, and inspections. In practice, the most consequential decisions -- process validation strategy, CDMO selection, technology transfer readiness, regulatory filing quality -- sit at the intersection of both. The CTOQ role acknowledges that intersection and puts one leader accountable for the full manufacturing-to-quality continuum.

Boards haven't caught up. Even as companies consolidate CMC and quality under a single operating leader, boards continue to treat manufacturing and quality expertise as operational detail rather than governance competency. An executing function, not a strategic one.

A CEO reports the CDMO relationship is "on track." The clinical and financial directors hear a status update. A director with CMC and quality experience hears unanswered questions:

Is the quality agreement finalized, or is the company operating on a draft that hasn't been stress-tested against an FDA inspection?

Does the technology transfer protocol include defined acceptance criteria, or is the CDMO interpreting "successful transfer" on its own terms?

Is the CDMO's deviation and CAPA system mature enough to catch process drift before it becomes a batch failure, or is the sponsor inheriting a reactive quality culture?

Outsourcing transfers activity, not risk. Without CMC and quality expertise in the room, the board can't evaluate whether the sponsor's oversight will hold up to the standard the FDA will apply.

The team presents a manufacturing cost projection for commercial scale. The financial director evaluates the number. A director with CMC and quality experience evaluates what's missing:

Does the projection include process characterization studies -- the work required to define critical process parameters and proven acceptable ranges before validation can begin?

Does it account for the three consecutive validation runs at commercial scale, including raw material procurement, facility time, and analytical testing each run requires?

Does it include the comparability data package required if the company ever needs to change manufacturing sites -- a scenario that isn't hypothetical when you're dependent on a single CDMO?

These gaps aren't rounding errors. Process characterization, validation, and comparability work can add 12 to 18 months of timeline and tens of millions in cost. They're frequently excluded because the people building the projections don't have the manufacturing and quality experience to know what's missing.

The board reviews a risk register that categorizes manufacturing as "medium risk -- outsourced to experienced CDMO." A director with CMC and quality experience sees a different picture:

Is process robustness being measured by defined critical quality attributes, or is the company equating "batch success" with "process control"?

Is the quality system built on preventive controls and CAPA trending, or is it reactive -- catching problems after they reach deviation reports?

Has anyone evaluated what happens to the supply chain if the primary CDMO site receives a Form 483 observation that requires remediation? Is there a qualified backup, or does a single observation shut down the program?

A risk register that says "outsourced to experienced CDMO" tells you the activity has been placed. It tells you nothing about whether the oversight is adequate, the process is robust, or the quality system is resilient.

A non-employee director seat on a private biopharma board costs $25,000 to $50,000 per year in cash retainer, plus an equity grant vesting over three to four years.

Now consider what the company spends when the expertise is missing and the problems arrive:

Form 483 remediation: $250,000 to $12 million in direct costs, with teams of 10 to 30 consultants working for 6 to 12 months

FDA Warning Letter: $250,000 to $125 million -- the industry benchmark is a minimum of 15% of business unit revenue -- with teams of 30 to 70+ consultants for 12 to 18 months

Complete Response Letter: $10 million or more per month of delay, with a median of 1.28 years to approval and $600,000+ per day in lost commercial opportunity

Clinical hold (manufacturing or quality related): $1 million to $10 million per month in burn while the program sits idle, with potential loss of clinical sites and enrolled patients

The arithmetic isn't subtle. A single Form 483 remediation can cost more than a decade of board seat retainers. A Warning Letter can consume more capital than most Series A rounds. The consultants who staff these remediation teams are often the same people who could have been advising the board proactively. The difference is whether you pay for that expertise at $50,000 a year or at emergency rates multiplied across 70 people for 18 months.

Acquirers price CMC and quality risk whether boards measure it or not. Their technical operations and quality teams evaluate specific questions during diligence:

Is the manufacturing process fully characterized and validated at commercial scale?

Is the quality system mature enough to pass a pre-approval inspection without generating observations that delay approval?

Does the quality organization have the depth and documentation to operate independently of any single individual?

They adjust the offer based on what they find. They structure contingent value rights when they find gaps.

A board that has never asked these questions sends the company into diligence unprepared. The acquirer's team identifies gaps the board didn't know existed, and every gap becomes leverage. The purchase price adjusts downward. The earnout structures get more aggressive. The contingent value rights expand. The company's shareholders absorb a discount they never saw coming because the board was never equipped to see it forming.

A board that has been asking CMC and quality questions for two or three years enters diligence in a fundamentally different position. The manufacturing dossier is more robust. The CDMO relationships are contractually tighter. The quality system has been pressure-tested by someone who knows what an FDA investigator will look for. That board doesn't give the acquirer a discount -- because there's no information asymmetry to exploit.

The CTOQ trend tells us something important. Companies are recognizing that CMC and quality are a unified strategic discipline. Boards that add this expertise gain the same advantage at the governance level that operating companies gain when they consolidate under a CTOQ.

It takes one board seat. The return shows up in the exit conversation, which, for most venture-backed biopharma companies, is the conversation that matters most.

Don't let the acquirer's diligence team be the first CMC experts your board has ever encountered. By then, you're negotiating the discount, not preventing it.

We have a been building a governance framework for exactly this. If you want to talk more about your board structure and who can increase your exit value. Please DM me.

William Blair, Biopharma Outsourcing Report (2023-2024). FDA Pre-Approval Inspection Guidance. Pearl Meyer, Private Biopharma Board Compensation (2024). Compliance Architects, "The Dollar Cost of a Warning Letter" (2023). Spencer Stuart Board Index (2025). The FDA Group, FDA Form 483 Response and Remediation Services. Applied Clinical Trials, "How Much Does a Day of Delay Really Cost" (2023).

Every engagement begins with a diagnostic — a structured read on the role and the company you are actually inheriting.

Start a diagnostic